Financial advisors in Troy NY

Helping you prepare

for your financial future

We're a team of investment advisers committed to protecting the financial future of our clients.

We're a team of investment advisers committed to protecting the financial future of our clients.

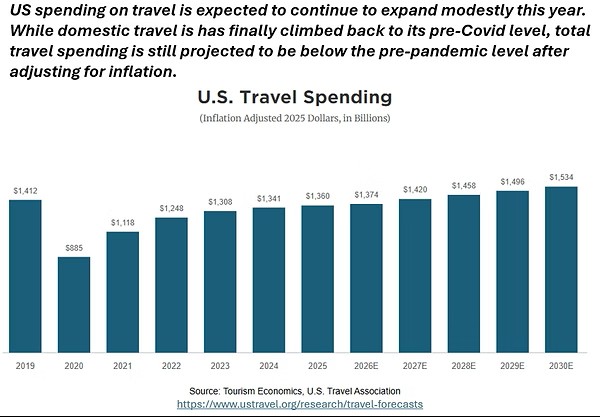

For many Americans, taking a summer vacation is a rite of passage. Whether you head to the beach or the mountains, or anywhere in between, most of us enjoy taking time away from our busy lives to reset and reconnect with family and friends. When it comes to consumer discretionary spending, traditionally vacation spending is one of the largest expenses. As such, travel trends can provide insight into the overall health of the economy. As the chart below from AO Wealth shows, overall spending on travel is growing steadily and not exhibiting any weakness that might be an early warning sign for the broader economy.

However, the period following the midterm election has historically been much stronger. Year three of the presidential cycle has generated an average return of 14.7%, the highest of the four years shown. One possible explanation is that election-related uncertainty begins to fade, while elected officials may focus on policies intended to support economic growth ahead of the next presidential election. Historically, it really doesn’t matter how the midterm election goes - Democratic sweep, Republican sweep, split Congress. Regardless of the outcome, the following year the S&P 500 returns, on average, anywhere between 10% and 15% and is positive roughly 88% of the time according to Sofi. The broader lesson is not that investors should attempt to time the market around elections. Although historical patterns can provide useful context, each market cycle is shaped by different economic conditions, including inflation, interest rates, corporate earnings, and geopolitical events.

“This presentation is not an offer or solicitation to buy or sell securities. The information contained in this presentation has been compiled from third party sources and is believed to be reliable, but its accuracy is not guaranteed and should not be relied upon in any way, whatsoever. Fagan portfolio characteristics and holdings are subject to change at any time and are based on a representative portfolio. Holdings and portfolio characteristics of individual client portfolios may differ, sometimes significantly, from those shown. This information does not constitute, and should not be construed as, investment advice or recommendations with respect to the securities listed.

Additional information including management fees and expenses is provided on our Form ADV Part 2. The actual return and value of an account fluctuate and, at any time, the account may be worth more or less than the amount invested. Bond Investments are affected by interest rate changes and the credit-worthiness of the issues held in the portfolio. A rise in interest rates will cause a decrease in the value of fixed income positions. Past performance results are not indicative of future results.”

Investing at New Highs

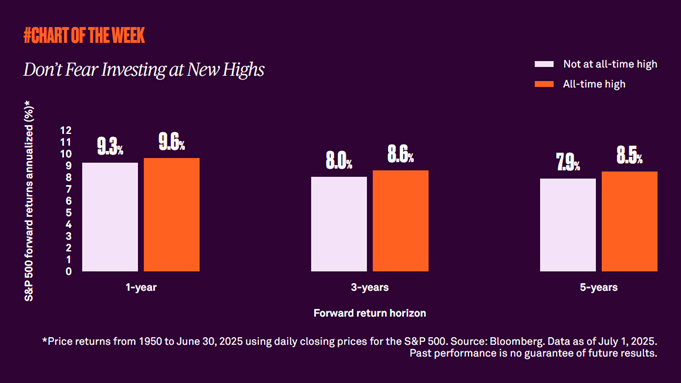

While the first half of 2025 has certainly been volatile, as previously noted here the S&P 500 has rebounded nicely and closed at a new record high as recently as last Thursday. The Nightly News (is that still a thing people watch?!) love to highlight when markets reach new highs, and a natural human response to that news is to wonder if now is a good time buy or should you wait for a pull back?

Chart courtesy of BNY/Wealth weekly insights

As the chart above from BNY Wealth illustrates, history shows that investing at new highs yields similar returns over a 1-, 3-, and 5-year lens as when you are investing at lower levels. Despite the “Nightly News” making a big deal out of all-time highs, they should be viewed just like any other trading day. Generally speaking, maintaining a long-term perspective is the most effective way to build wealth, and avoiding the “fear” of investing during any both good and bad market periods fits that narrative.

First and foremost, we believe that the pro-growth rhetoric upon which President Trump was elected has given way to perhaps the most protectionist administration in a century. The unintended results of the use of a tariff “shotgun” when a “rifle” should have been the appropriate metaphorical weapon of choice is currently reverberating throughout the financial markets.

That said, we expect either President Trump to shortly convey to investors that the imposed tariffs are part of a negotiating tactic or Congress to push back a bit against his current course of action. Either will stem the negative tide and help begin to cure sentiment.

Nonetheless, other than nibbling at the edges, there is too much uncertainty in the financial markets to make broad, sweeping commitments in the form of new purchases or wholesale sales. Moreover, there is a lack of meaningful clarity regarding what the tariffs levied by President Trump will ultimately mean for the global supply chain, domestic demand, inflation or for the potential for new alliances amongst our both our friends and adversaries.

What to do. Rely on the fact that your portfolio was designed prior to the recent volatility, unemotionally, and with your long-term objectives in mind.

Rely on the fact that stocks tend to pull back at least ten percent once every eighteen months and, according to data from the Schwab Research Center, since 1974 only six of the twenty-two such corrections have turned into bear markets (1980, 1987, 2000, 2007, 2020 and 2022). Furthermore, rely on the knowledge that bear markets occur approximately every four years so that if you retire at 63 and live 20 years, you can expect perhaps five bear markets during that time frame. They are part and parcel with investing for the long-term and are what provides the dry powder (to continue the weaponry metaphor) for long-term gains.

Rely on proper asset allocation and the knowledge for those investors that own bonds, economic slowdowns provide a tailwind.

Rely on the peace of mind that the cash in your portfolio provides. We recommend up to twenty percent for the jittery.

As of today, all of the major indexes have entered correction territory, which we define as at least a drop of ten percent from former highs and regardless of where the market goes over the short-term, as the chart below illustrates, ensuing market gains tend to be much longer and rewarding.

Data from 12/12/1961 to 2/19/2025, which is the current peak of the latest bull market. The market is represented by daily price returns of the S&P 500 index. Bear markets are defined as periods with cumulative declines of at least 20% from the previous peak close. Its duration is measured as the number of days from the previous peak close to the lowest close reached after it has fallen at least 20%, and includes weekends and holidays. Periods between bear markets are designated as bull markets. Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. Past performance is no guarantee of future results.

“This presentation is not an offer or solicitation to buy or sell securities. The information contained in this presentation has been compiled from third party sources and is believed to be reliable, but its accuracy is not guaranteed and should not be relied upon in any way, whatsoever. Fagan portfolio characteristics and holdings are subject to change at any time and are based on a representative portfolio. Holdings and portfolio characteristics of individual client portfolios may differ, sometimes significantly, from those shown. This information does not constitute, and should not be construed as, investment advice or recommendations with respect to the securities listed.

Additional information including management fees and expenses is provided on our Form ADV Part 2. The actual return and value of an account fluctuate and, at any time, the account may be worth more or less than the amount invested. Bond Investments are affected by interest rate changes and the credit-worthiness of the issues held in the portfolio. A rise in interest rates will cause a decrease in the value of fixed income positions. Past performance results are not indicative of future results.”